EDI in the Financial Services Industry

The introduction of technologies such as EDI has enabled the financial services industry to automate many of the day-to-day processes between counterparties.

Financial services firms provide a wide array of products and services to their clients, both retail and commercial, across commercial banking, securities, cards and merchant services, insurance and employer services. Particularly when supporting commercial clients, the industry relies on the ability to manage complex information flows whether processing payables and receivables, supporting post-trade securities flows, transmitting merchant settlement files, or enabling group benefits eligibility claims.

The growth of international trade has created interdependencies between buyers and suppliers across geographies, resulting in the globalization of the financial supply chain. Complexities arise when working across international boundaries, including differences in currencies, regulations and accounting practices. EDI mitigates these complexities by aligning financial supply chain information flows with the movement of goods in the physical supply chain. A fully automated financial supply chain enables the seamless, accurate and timely exchange of financial data between buyers, suppliers and their financial institutions.

With EDI, an organization can electronically receive an invoice and initiate a payment. Eliminating the paper in payables and receivables flows enables organizations to reduce days sales outstanding and days payables outstanding, optimizing their cash conversion cycles. EDI also provides a lower-cost alternative to traditional paper-based payment methodologies, while eliminating errors associated with manual processes.

Due to the global nature of the financial services industry, there are numerous file format and communications protocols in use today, along with a number of regional EDI networks. The structure of the financial supply chain and a description of the communication protocols and file format standards used are described below.

Supply Chain Structure

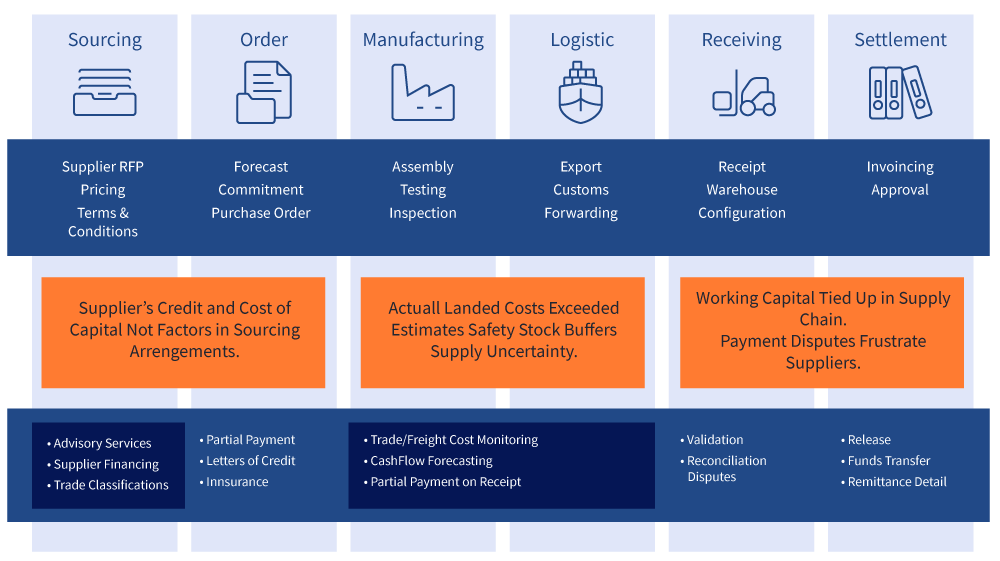

All industries use some version of a supply chain to track the flow of goods and services it uses and produces. Financial services is no different. Financial transactions are an integral component of the physical supply chain. By connecting business partners from order placement to settlement, the financial supply chain carries the flow of financial information in the direction opposite to the flow of goods and services.

The financial supply chain is one that is closely aligned with and triggered by processes in the physical supply chain as demonstrated by the diagram shown below. Financial supply chain services include transactions related to purchase order processing, letters of credit, open account management, pre & post-shipment financing, reconciliation, invoice presentment, dispute management, foreign exchange and insurance management.

Buying firms initiate the process when they source materials and/or finished goods from suppliers within their supply chain. Financial institutions may help advise the buyer on issues related to credit issuance and financing. Once an order is placed, the financial institution may provide partial payment against the negotiated terms or supply an approved letter of credit to show the supplier that the buyer has the means to pay once production begins. Once the goods are produced and shipped, the financial institution may help insure the goods and, upon receipt, settle the account according to the terms of the contract.

The financial institution may also help the buyer to forecast cash flows using cash management services it provides to the buyer. The financial institution may also help to reconcile disputes, validate data related to the goods, and finally release funds and remittance detail.

Communication Protocols Used

EDI is widely used by commercial firms to initiate transactions with their financial services counterparties. EDI facilitates financial supply chain transactions such as the direct deposit of payroll checks by employers, the direct debit of consumer accounts, and the electronic payment of government taxes by businesses. With the increasing emphasis on security, the financial services industry has added a number of secure communication protocols along with the more common ones used for other industries.

While many organizations use FTP and FTPs, others use AS2, OFTP, ZENGIN, HTTP/S, MQ Series, and VPNs. The Financial Information eXchange (FIX) protocol is an electronic communications protocol initiated in 1992 for international real-time exchange of information related to the securities transactions and markets. In Europe, specifically in France and Germany, EBICS has gained some acceptance as the transmission protocol for corporate-to-bank communication using the XML format which supports the Single Euro Payments Area (SEPA) initiative to standardize clearing protocols in the interbank networks.

Document Standards Used

In addition to traditional EDI formats such as ANSI X12 and UNI/EDIFACT, other popular standards for treasury, cash management and securities are ISO 20022 XML, NACHA, BAI2, SAP IDOC, Microsoft Excel, SWIFT MT/FIN, FIX XML, FpML, and ISO 15022.

For international financial messaging and bank-to-bank communications, SWIFT is the dominant worldwide standard. SWIFT is a member-owned cooperative that includes more than 10,000 around the world including central banks like the Federal Reserve, regional payment systems, commercial banks, securities firms and more recently, corporations.

Standards are a core element of SWIFT’s services. SWIFT develops and defines messaging and standards for the financial services industry, enabling communication and collaboration between financial counterparties. SWIFT provides standards financial messaging including payments, trade services, securities and corporate actions. The most common SWIFT message standards are MT and MX.

Industry Associations

Due to the financial crises in the late 2000s, the industry organizations that help automate, standardize and centralize financial data are more widely known than ever. There are numerous industry associations and standards setting bodies around the world that influence the standards, communication protocols, file formats and technology architecture exchange information electronically between financial institutions and their clients. Some of the most widely known standards organizations include SWIFT, AFP, ISO, NACHA and SWIFT.

The International Organization for Standardization (ISO) is an international-standard-setting body composed of representatives from various national standards organizations. Founded on 23 February 1947, the organization promulgates worldwide proprietary industrial and commercial standards including the emerging ISO 20022 standard widely used across financial services. ISO has its headquarters in Geneva, Switzerland.

NACHA is a national, not-for-profit organization that develops operating rules and business practices for electronic payments. Members of this organization define the rules covering the Automated Clearing House (ACH) network in the United States. While NACHA has largely set the standards for low-value electronic payments for in the United States, there are numerous global variants governing domestic low-value payments systems.